Truckload Performance in November 2021

November 2021 - Transportation Market Report

What's new in the TL Space?

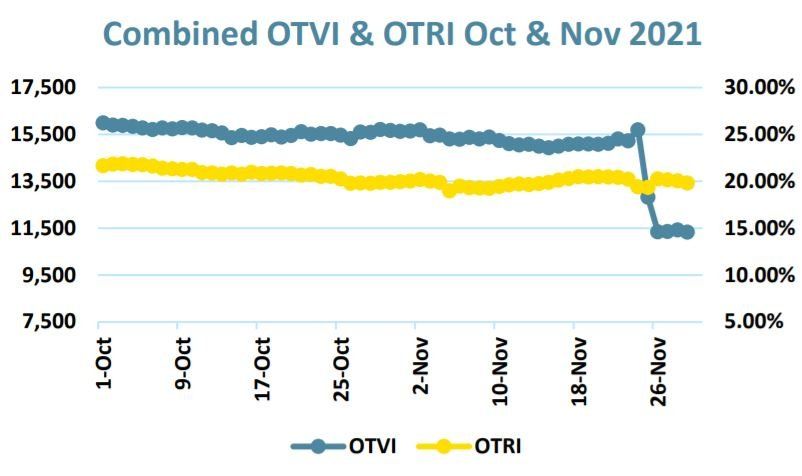

- The markets performed as they historically have in November:

- Volumes stayed relatively flat before spiking right before Thanksgiving week.

- Rejection rates held around the 19% to 20% range. We are hopeful there could be a drop in late Q4, early Q1.

- Multiple business groups including the American Trucking Associations (ATA) filed a lawsuit on Nov. 5, to block the upcoming vaccine mandate. ATA estimates that the industry could lose up to 37% of large carriers' drivers if the challenge fails in the courts.

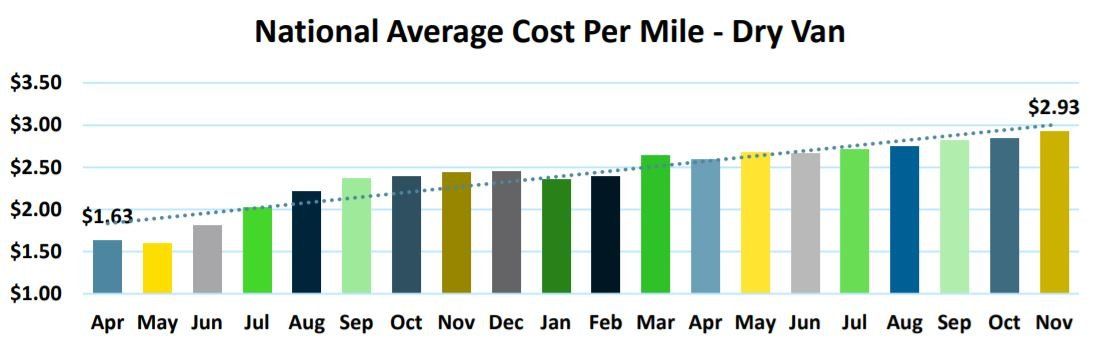

Dry Van: Load To Truck (LTT) & Cost Per Mile (CPM)

- In early November rates remained flat but going into Thanksgiving week we saw a spike as carriers started to take their trucks off the road.

- There’s no indication of a let-up in terms of volume for the balance of 2021. Import volume projects will remain extremely high and domestic manufacturing is expected to remain strong.

- With import volumes remaining strong, we would expect capacity to remain tight and costs to continue to rise for OTR volumes near major import gateway locations. The industrial sector could theoretically slow due to raw material/input shortages, but we do not expect that to make a material difference in terms of costs and capacity.

Key Takeaway:

Volumes are not expected to drop through 2021, and most likely at least Q2 2022. Capacity will remain further constrained in major markets located near major import gateways. Fuel surcharges are the leading contributor to what is driving the spike as we end the month. We are optimistic regarding the CPM at least staying flat with the recent announcements of the Biden administration releasing oil reserves and the OPEC+ surplus building.

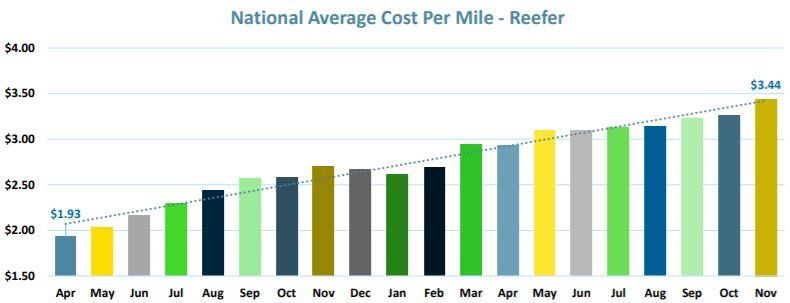

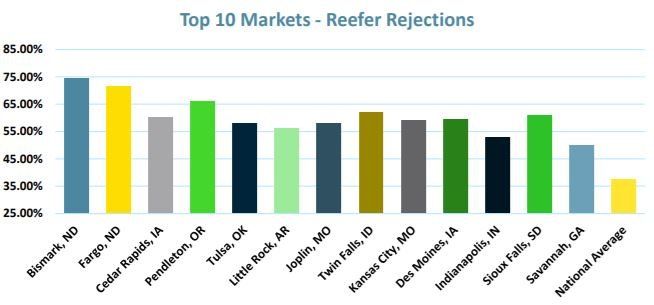

Reefer: LTT & CPM

- The reefer space remains extremely tight in terms of capacity with elevated rates.

- We do not expect rates or capacity to improve in the balance of 2021.

Reefer: Outbound Tender Volume (ROTVI) & Outbound Tender Rejection (ROTRI)

- The Reefer LTT remains significantly elevated vs. both 2020 and 2019. There’s no end in sight in terms of loosened capacity or a regression in rates.

- Reefer volumes dipped at the end of the month due to the Thanksgiving holiday, but we expect volume to rebound immediately with protect from freeze.

Key Takeaway:

We do not expect rates or capacity to improve in the balance of 2021.

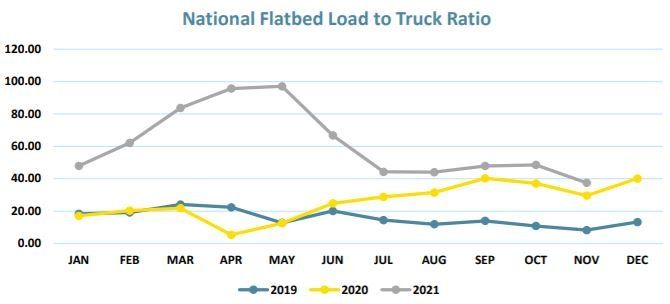

Flatbed: LTT, CPM and FOTRI

Flatbed utilization will continue to remain strong. Housing Starts Privately‐owned housing starts in September were at a seasonally adjusted annual rate of 1,555,000. This is 1.6 percent (±11.4 percent)* below the revised August estimate of 1,580,000, but is 7.4 percent (±13.0 percent)* above the September 2020 rate of 1,448,000. Single‐family housing starts in September were at a rate of 1,080,000; this is virtually unchanged from (±8.4 percent)* the revised August figure of 1,080,000. The September rate for units in buildings with five units or more was 467,000.

Key Takeaway:

We anticipate Flatbed costs and capacity to remain elevated and restricted for the coming months. Construction volumes should remain high (steel, lumber, equipment), the manufacturing sector continues to improve.

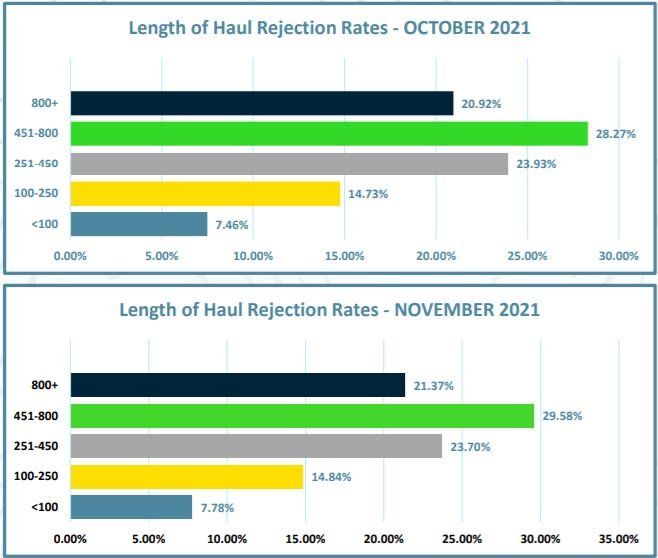

Domestic TL Length of Haul Rejections

This measures the Rejection rate at specific lengths of haul. We saw slight progression in rejections for all lengths of haul.

Key Takeaway:

The “Tweener” lane continues to have the highest Rejection rate by category. Previously, drivers could make the 450+ mile runs in a day. Due to HOS regulations, they are no longer able to do so. Ensure you are providing more than adequate lead time, and ensure appointments are set at both the shipper and receiver.

Click the button above to receive the full transportation market report for November 2021.